PRINCIPLES OF FOOD & BEVERAGE COST CONTROLS

The Importance of Cost Control

It is important for any operation, especially restaurant and foodservice operations, to continuously monitor and control its costs of operation. These include production and service, labor, utilities, and marketing. The average establishment shows a very small profit and the difference between the bottom line of a financially successful operation and that of a failed business is only around 3 or 4 percent.

Sales - expenses = profits

Types of Costs:

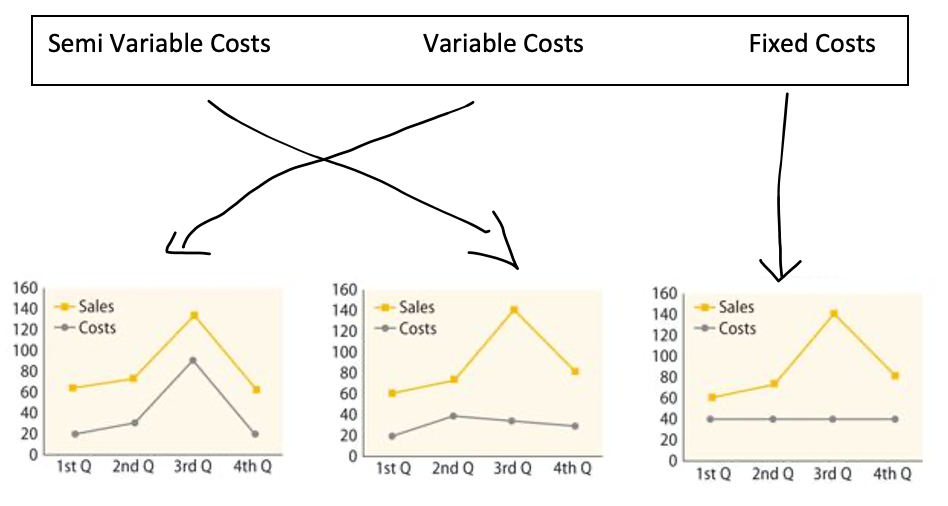

- Fixed costs: Those costs that remain the same regardless of sales volume

- Variable costs: Costs that increase and decrease in direct proportion to sales

- Semivariable costs: Costs that increase and decrease as sales increase and decrease but not in direct proportion

- Controllable costs: Costs that the manager can directly control

- Noncontrollable costs: Costs over which the manager has little or no control

The relationship between cost and profitability: Cost goes up, profitability goes down. If we keep costs down, profitability goes up.

As business owners, you have to find that fine line. We don’t want to lower costs so much that we sacrifice the quality of the product because then no one would buy it.

Sales – expenses = the profit or loss. Always do sales first.

Sales = $25,000, Expenses = $20,000. 25,000-20,000 = $5,000

Sales = $15,250, Expenses = $15,350. 15,250-15,350 = -$100

Three different types of cost.

Fixed Costs: Stays the same. Doesn’t matter how much is made. Rent, insurance, salaries

Variable Costs: Rises and lowers in relationship to sales. As sales increase, costs increase. More customers to feed = spending more money on food. Examples include wages (hourly employees, food & beverage-the ingredients).

Semivariable Costs: Comprised of both fixed and variable costs. Labor as a general term includes salaries and wages (hourly).

Controllable Costs: Variable

Noncontrollable Costs: Fixed

Prime cost = food cost, beverage cost, and labor cost (these are the most controllable costs).

Calculating Prime Cost

Food Cost

+Beverage Cost

+Labor Cost

=Prime Cost

Food and Beverage is usually about 30-33%. Labor is 30-35%.

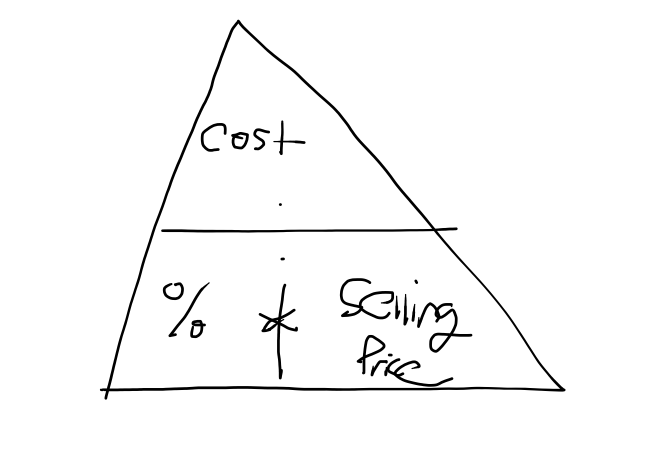

Calculating Food Cost

(The triangle)

The lemons – saving a lemon by asking the customer if they want a lemon.

250 teas in a day

x 30% of people who don’t like lemon with their teas

--------

75 people are going to take the lemon and put it on the side

If a lemon has 6 slices, and the lemon costs .60 each....which is .10 per slice.

75 people x .10 = $7.50 x 360 days open a year = $2,700

Variance = the Actual vs. Budgeted. A minus B. That is the variance. What actually happened minus the budgeted.

Food sales budgeted $100,000 but brought in only $90,000. Percentage is –10%

If costs were also down 10%, then that’s an OK number. If costs are high and sales down, then that’s bad. It just depends. Look at the whole picture.

Budgeted

Actual Sales

Difference

Variance

-----------------------------------------------------------------------

$250,000 $275,000 $25,000 Difference/budgeted number = .10, 10% over budget

275,000 Actual – 250,000 Budgeted = 25,000. Then the difference, the part, divided by the whole number.

----------------------------------------------------------------------

750 Covers 680 Covers -70 -9.3%

If each table had apps, then even though the covers were down, the sales were steady or up

- How do costs affect profit. Provide 1 example (that is not provided in the book) of how controlling costs can affect profit.

- It takes money to make money, but cost can affect profit in a profound way in the hospitality setting. If the cost is too much, no profit is made. If the cost can be controlled, then the bottom line will see the benefit. One example of controlling costs that might affect profit is developing a recipe that maintains quality but might use different, less expensive ingredients to make. Therefore, the reduction in the cost of the product – an appetizer for example – would impact the profit margin in a positive way.

- What is the manager's role in establishing cost controls?

- A manager will be able to set the example for everyone in the facility. Someone who is positive, upbeat, and pays attention to details will be able to maintain a happy work environment while also providing the establishment with an effective way to produce the highest standards and maintain strict cost controls. The manager sets the tone. That means the manager can step in and correct things when he or she sees them happening. This will be the best way to change course quickly.

- Please provide one example of a:

- Fixed Cost – the rent of the building

- Variable Cost – hourly employees

- Controllable Cost – staffing level

- Non-controllable Cost – price of eggs

- Why is Labor Cost considered semivariable?

- Labor comprises both fixed and variable aspects. The employee’s wage is set, but the manager may control how much the employee is on shift depending on restaurant volume.

- What is the universal formula for %?

- % = Part / Whole x 100

Fixed Costs are costs that remain the same regardless of sales volume. Insurance is a good example. The policy cost will remain the same throughout the term. Variable costs increase and decrease in direct proportion to sales. Food cost is an example. As sales increase, more food is purchased to replenish inventory. With adequate controls, there is little waste or theft. Semi-variable costs increase and decrease as sales increase and decrease, but not in direct proportion. It's made up of both fixed costs and variable costs. Labor cost is an example. Managers are normally paid a salary that remains the same regardless of the operation's sales volume. On the other hand, waitstaff and line cooks are paid hourly wages and are scheduled according to anticipated sales. As a result, the cost of hourly staff increases as sales increase - and decrease as sales decrease.

Controllable costs are those that the managers can control. One example is food cost. Managers can use standardized recipes for portion control, menu listing, and pricing. Labor is also a controllable cost. By changing the number of hours an employee works, a manager can affect labor costs.

Prime Cost is the operation's total food cost, beverage cost, and labor costs for a specific time period, usually a week or month.

Prime cost = Food Cost + Beverage Cost + Labor Cost

- In your own words, describe the relationship between cost and profitability.

- Profitability is what is left after all of the expenses have been paid such as the materials for the recipes and the labor. Cost is what takes away from the profit margins but is necessary to run the business and maintain quality.

- Calculate the profit or loss

- Sales = $25,000 and Expenses = $20,0000

- $5,000 profit.

- Sales = $15,250 and Expenses = $ 15,350

- Loss of -$100.

- Draw a line to connect the term to the appropriate chart

- Create a list of controllable costs.

- Food & Beverage

- Wages/labor

- Marketing

- Supplies

- Create a list of Non-controllable Costs

- Rent for the building

- Utilities

Permits or licenses needed

- Prime Costs include __food cost_____, ___beverage cost____, and __labor costs_____.

- Food cost % is the relation of ___cost____ to __selling price______.

8. Draw the tool discussed in class to easily calculate Food Cost %, Menu Price, or Recipe Cost

- To use the tool above, you __cover up______ what you are looking for, and fill in the remaining information.

- Complete the following equations.

- Food Cost = % x selling price

- Food Cost % = cost / selling price

- Selling Price = cost / %

- __Variance___ is the difference between budgeted and actual performance.

- To determine the Variance %, follow the steps below:

- Actual Performance – Budgeted Amount = Variance

- Variance / Budgeted Amount x 100 = Variance %

Chapter 2 - Forecasting & Budgeting

Forecasting is predicting the future based on what happened in the past. Forecasting increases or decreases by percentages.

Increasing By %

- Multiply the original number by %

- Add the answer to the original number

Decreasing by %

- Multiply the original number by %

- Subtract the answer from the original number

Increase 3%

From 2,000 guests = 2,000 x .03 = 60. Add to the original number = 2,060 guests.

Increase 2.5%

From 5,000 = 5,000 x .025 = 125. Add to 5,000 = 5,125.

5,000 x 1.025 = 5,125 because that gives you the x100 already

Decrease 5%

From 15,000 = 15,000 x.05 =

Decrease 1.5

From 1,200 x .015 = 18. 1,200 – 18 = 1,182.

1,182 – 1,200 =

Income Statements

Sales is always 100%.

Sales $3,000,000

Food Costs 25%

Bev. Costs 15% all of this equals 100%

Gross Profit

Labor cost

??

Other Exp 21%

Profit 11%

P/L = sales – expenses

Sales = profit + expenses

---

Ch. 2 continued – 9/8/25

Corrective actions toward the end of the budgeting process.

Line Item Review – look at each line by line.

Sales = $1,300,000.00 budgeted; actual is $1,400,000.00; variance is $100,000.

Variance is 7% taking 100,000 variance divided by sales of 1,300,000.00

Gross operating profit is how well we’re controlling our food cost. (Net profit is at the bottom of P&L accounts for other expenses, etc.)

Another example:

Sales, met budget.

Food and beverage, spent 50k more than we budgeted – up 3.8%

Labor cost, no change.

This is a bad situation because food is one of the most controllable costs.

Review

- A budget is a __plan that shows financial objectives or standards.________.

- Forecasting________________ is used when preparing a budget.

- Increasing by a %

- Multiply______ the original number by the %

- Add____ to the original number

- Decreasing by a %

- Multiply_____ the original number by the %

- Subtract____ from the original number

- Profit and Loss Statement____ is a snapshot of a business’s profitability, also know as an Income statement

- First line of the P&L __Sales__________

Second line of the P&L _Food and Beverage Costs________________

Third Line of the P&L___Gross Operating Profit/Payroll____________

Fourth Line of the P&L __Other______

Bottom Line of the P&L___Profit/Loss_____

- Sales always represents __100% - the whole_____

- All costs % + profit % added together equals _total cost of sales____.

- The final two steps in the budget process _evaluation/analyze__ and __corrective action____.

Chapter 3 - What is food cost?

What we spend on the ingredients – the cost to make the item or beverage.

It becomes a part of our cost when it’s in production. A 50 lb bag of flour is not counted as a food cost until it’s being put to use in something.

Calculating Basic Food Cost (formula)

Beginning Inventory

+ Purchases for the Period

- Ending Inventory

--------

Cost of Goods Sold (CoGS).

In the triangle, the C is the cost at the top.

Beginning inventory 2,500

Purchases

Total available inventory

Ending inventory

$ costs of goods sold

Transfers

Food-to-bar transfer

Cost Transfers from Other Units

Cibolo Moon-chicken wings High Velocity Bar

Wings have to be transferred from Cibolo Moon to High Velocity Bar if the bar needs the wings

Standardized Recipes

Cost consistent – advantages to using standardized recipes... the quality, the quantity, the product specifications.

Portion sizes

Weight – proteins, some sides, apps

Volume – drinks, soups, sauces/dressings

Count – eggs, desserts, wings/tenders, apps

A salad – the lettuce, 4 oz is by weight. Tomatoes, croutons could be count... the dressing is volume.

Costing out standardized recipes

Cost

--per--

Unit

Calculating Food Cost

Converting AP quantities into EP quantities

As Purchased (AP) = 10 lbs of bell peppers

EP = 8.5 lbs of bell peppers

EY % (edible yield, what’s left over after trimming, dicing, etc) =

(equation part divided by whole)

AP = 25 lbs of bell peppers

EP = ?

EY % = 85%

Now we need 35 lbs

AP = ?

EP = 35 lbs of bell peppers

EY % =

Watch brisket math video for Wednesday.

Review

Food only becomes part of Food Cost when ____it goes into production/when it is actually used__________.

The Formula for calculating cost of food sold is:

Beginning Inventory + Purchases - Ending Inventory = Cost of Food Sold (CoGS, cost of goods sold)

Divide COGS by total food sales x 100.

2. Food ingredients are considered beverage cost when __an item might be transferred to the bar to be used in a __drink__

3. Beverage ingredients are considered food cost when __the item like a lime or strawberry used for a drink is transferred to the kitchen to be used in a __dish___

4. When calculating transfers you have to:

a. __Subtract______ the amount from the original location.

b. __Add______ the amount to the new location.

5. List the advantages to standardized recipes discussed in class. Consistent tasting dishes, able to control costs, and increases productivity.

6. Portions can be controlled by __quality___, ___quantity___, and __product specifications____. Or weight, volume, count.

7. __Edible portion (EP)_____ refers to the amount left over after processing.

8. __As purchased (AP)_____ refers to the amount of product delivered.

9. ___Yield factor______ refers to a % of usable product.

Chapter 4 - Determining Menu Prices

How much should we sell our products for? There’s not just one fixed way to do things.

Pricing is determined by four things:

Market-driven pricing (competition)

Demand-driven pricing (airports, concert venues)

Price-value relationship (finding value in it)

Markup differentiation

To determine pricing on a menu, etc, do the following:

-Triangle method

-Factor method (whatever it costs multiply by 3) (100/ideal %). To find 40%, 100/40 = 2.5. $15.25 (example) x 2.5 = $38.13.

-Contribution margin method, take all non food costs + ideal profit / number of guests = CM per guest _____. Add contribution per guest + food cost = menu selling price

non-food costs of 5,000, profit 3,000 = 8,000. There are 2,000 guests = $4 per guest. $4 + 2.50 recipe cost = 6.50, etc.

-Q Factor Method: all the free stuff that comes with your item like 2 sides. The cost of the sides is built into the cost of the recipe. BBQ plate, a starch, vegetable, salad... plus jalapenos, butter... all of that is added up together. Like $3.43. No matter if someone orders sausage, turkey, brisket, you add the Q factor of $3.43 to the cost of the menu item. Mayonnaise packets, ketchup, napkins.

There’s a whole psychology around menu pricing. 9.99 vs. 10. Many people focus on that first number of 9 vs. 10.

- What 4 external factors affect menu prices?

- Competition/Market Driven Pricing___

- Price value relationship (guests have to find value in it)_____________________

- Markup differentiation__Not every item is created equal. The higher the cost of the menu item, the lower the markup can be.___________________

- Demand-driven pricing (airports, concert venues)_____________________

- 4 methods to determine menu selling price include:

- Triangle______________________________

- Factor method – whatever it costs multiply by 3_________________________

- Contribution margin method______________________________

- Q Factor______________________________

- To calculate the Food cost % method we will use the ______ tool. Triangle

- To calculate using the Factor Method, we need to:

- Divide by the desired percentage to get the factor.

- Then ____multiply________ the recipe cost by the factor.

Example:

$2.50 Food Cost and a 20% target FC%

a. 100 / 20% target food cost = 5 (the factor number)

b. $2.5 x 5 = $12.5

- To calculate using the contribution margin method we need to:

- Add __Non Food Costs_________ and ___Profit____________

- Divide________ by the number of guests

- Add the Contribution margin per guest to the recipe cost

Example:

$5000 Non Food Cost and a $3000 profit 2000 guests

a. $5,000 (rent, insurance) + $3,000 (profit) = $8,000

b. Divide by 2,000 guests = $4 per guest

c. + Recipe costs: + $2.50 = $6.50; + $3.00 = $7.00; + $15.25 = $19.25; + .15 = $4.15

- The ___Q Factor_____________ refers to the total of all similar complementary items in a plate.

All of the “free” stuff that comes with the menu item. Entrée + two sides. Ketchup packets. - The ___profit______ is the difference between the selling price and the recipe cost.

- To find the average Contribution Margin, we need to:

- Add___________ all the contribution margins together

- And then _____divide___________ by the number of items on the menu.

- The ______popularity_________________ or ____contribution margin___________________ refers to how popular an item is on the menu.

- To Find the Popularity Benchmark, we need to:

- Divide ___100_____ by the number of items on the menu

- Then __multiply________ by the Popularity factor provided.

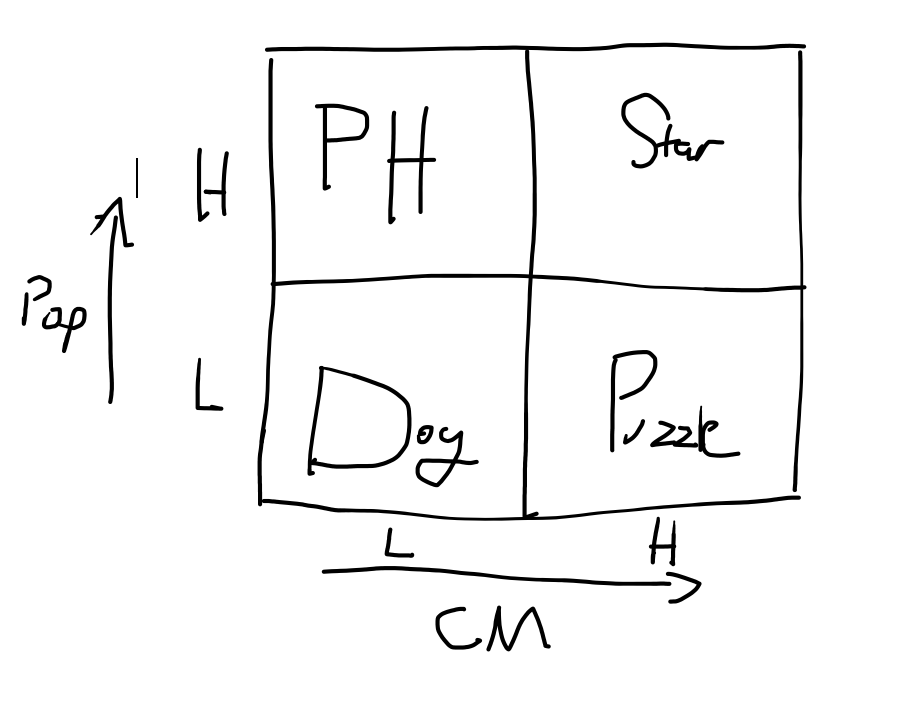

- Draw the menu analysis diagram discussed in class.

High contribution high popularity = star

High proft and low pop = puzzle

Chapter 5 - Controlling Food Costs in Purchasing

Purchasing is one of the key areas in the cost control process.

Par level means an operation has enough stock on hand to get the kitchen through until the next order is delivered.

12 cases of green beans is par level - 4 cases that are left in stock = 8 cases to order

When placing an order, the manager looks on the par sheet to determine the quantity currently on hand. This is called perpetual inventory and is used rather than taking a physical inventory.

- Draw the Purchasing Cycle below

- When purchasing we need to know the __Inventory______

- Product Specifications are divided in two categories __Quality____ and __Quantity____.

- Ingredient Example_____________________

Quality Quantity

15 lb

- PAR level__________ is the minimum amount needed on hand for normal operations.

- Establishing PAR

- (Similar Daily Usage)_____________ the daily Usage by the number of days between deliveries.

- (Different Daily Usage)_____________ the daily Usage for days between deliveries.

Chapter 6 - Receiving, Storing, Issuing

Receiving is an area in the foodservice operation that gets little attention.

List required tools for receiving food and beverage orders.

- Thermometer

- Scissors

- Time piece

- Sheet/list

- Purchase order

- Dolly

- Scale

- Staff

- Pen/marker

- Receipt

- Box cutter